- Fed rate hike, Powell press conference, CPI inflation data in focus.

- Oracle shares are a buy with earnings on deck.

- Adobe stock set to struggle amid weak outlook.

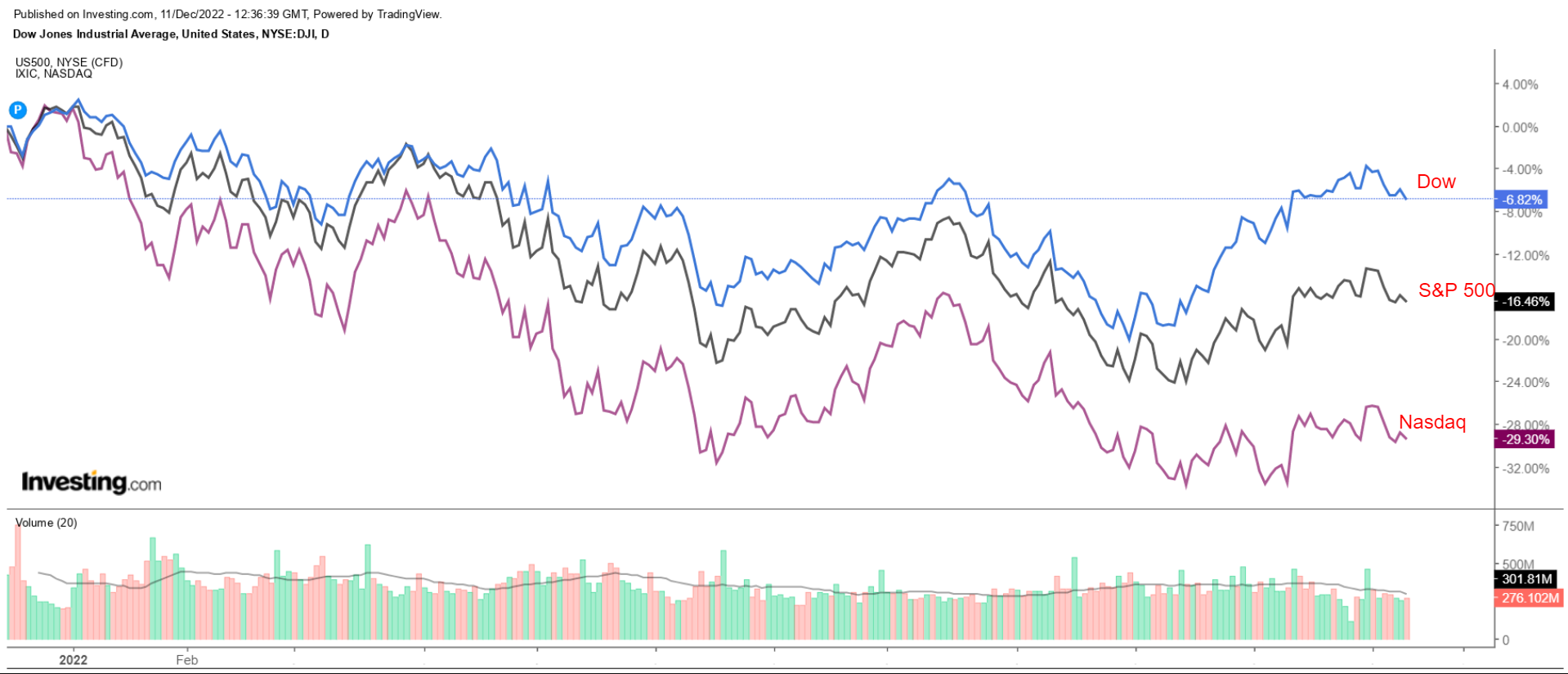

Stocks on Wall Street declined on Friday, with the major indices wrapping up their worst week since September amid ongoing concerns about further rate hikes and a possible recession.

For the week, the blue-chip Dow Jones Industrial Average dropped 2.8%, while the benchmark S&P 500 and technology-heavy Nasdaq Composite fell 3.4% and 4% respectively.

Source: Investing.com

The coming week is expected to be another volatile one, as investors brace for two of the biggest economic events that remain for 2022.

The Federal Reserve will announce its rate decision at its last meeting of the year on Wednesday. A 50-basis-point rate increase by the central bank is seen as the most likely outcome, a step down from its recent series of 75bps rate hikes.

Fed Chair Jerome Powell’s comments on the pace of future rate increases will be in focus as I expect him to push back once more against the idea of a dovish pivot.

Meanwhile, on the economic calendar, most important will be Tuesday’s U.S. consumer price inflation report for November, which is forecast to show annual CPI climbing 7.3%, slowing from the 7.7% increase recorded in October.

In addition to the Fed and the CPI reports, retail sales data, the Philadelphia Fed’s manufacturing survey and the Empire State manufacturing survey will also be closely watched this week.

Regardless of which direction the market goes, below we highlight one stock likely to be in demand and another that could see further downside.

Remember though, our time frame is just for the upcoming week.

Stock To Buy: Oracle

I believe Oracle's (NYSE:ORCL) stock will outperform in the coming week, with a potential breakout to new multi-month highs on the horizon, as the software giant is forecast to deliver strong earnings and revenue.

As per moves in the options market, traders are pricing in a potential swing of approximately 8% in either direction for ORCL stock following the earnings update.

Source: InvestingPro+

Consensus expectations call for the Austin-based tech behemoth to post a profit of $1.17 a share when it releases fiscal second-quarter numbers after the closing bell on Monday, Dec. 12.

Revenue is anticipated to jump 16% year over year to $12.01 billion, reflecting strong growth across its key business segments. If confirmed, that would mark Oracle’s highest quarterly sales total in more than eight years, dating back to Q2 2014, as its ongoing transition to the cloud continues to pay off.

In my opinion, Oracle’s update regarding the performance of its cloud services and license-support segment will surprise to the upside to reflect growing demand from both large enterprises and government agencies. The key metric easily topped expectations in the last quarter, rising 14% on an annual basis to $8.42 billion.

As a result, I believe the company will provide an upbeat outlook for the current quarter as it remains well-positioned to shine despite a difficult macro environment.

Source: Investing.com

ORCL stock closed at $79.86 on Friday, within sight of its 2022 peak of $89.58 touched on Jan. 4. At current levels, Oracle has a market cap of around $215.3 billion.

Year to date, shares are down “just” 8.4%, much better than the 33.6% decline suffered by the Software & Services Select Sector SPDR Fund (NYSE:XSW), which tracks an equal-weighted index of software and services companies in the S&P 500.

Stock To Dump: Adobe Systems

Sticking with software companies, I expect Adobe (NASDAQ:ADBE) to suffer a difficult week ahead as the struggling tech giant’s latest financial results are forecast to fuel further concerns over its long-term outlook.

Earnings have been catalysts for outsize swings in ADBE this year, per data from InvestingPro+: When the company last reported quarterly numbers on Sept. 15, shares plunged 19.4% to suffer their worst day since 2010.

According to the options market, investors expect another sharp swing in Adobe’s stock following this week’s results, with a possible implied move of 7.7% in either direction.

Source: Investing.com

The San Jose, California-based company is projected to report earnings per share of $3.50 on revenue of $4.53 billion when it releases fiscal fourth-quarter numbers after the market close on Thursday, Dec. 15, according to Investing.com.

Beyond the top and bottom line, I believe there is downside risk that Adobe will issue guidance for the next fiscal year that could fall short of expectations amid slowing demand for its wide array of subscription-based digital media and marketing-software tools.

Adobe’s all-important Creative Cloud business is expected to have suffered another sluggish quarter as individuals and enterprises seek out cheaper options offered by some of its competitors, including Google operator Alphabet (NASDAQ:GOOGL), IBM (NYSE:IBM), and Oracle.

In addition, I’ll be curious to hear any further developments regarding Adobe’s pending $20 billion takeover of cloud-based design platform Figma as investors grow increasingly nervous over the rich price tag of the planned acquisition.

Source: Investing.com

ADBE ended Friday’s session at $330.64, earning it a valuation of $153.7 billion. Year to date, shares are down 41.7% due to a toxic combination of various macro and fundamental headwinds, including rising interest rates, lingering inflationary pressures, mounting recession fears, and changes to foreign-exchange rates resulting from a stronger dollar.

Disclosure: At the time of writing, Jesse has no position in any stock mentioned. The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.

Which stock should you buy in your very next trade?

With valuations skyrocketing in 2024, many investors are uneasy putting more money into stocks. Unsure where to invest next? Get access to our proven portfolios and discover high-potential opportunities.

In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. That's an impressive track record.

With portfolios tailored for Dow stocks, S&P stocks, Tech stocks, and Mid Cap stocks, you can explore various wealth-building strategies.