3 reasons why gold prices are surging again

Introduction & Market Context

Workiva Inc (NYSE:WK) presented its Q2 2025 investor update on July 31, 2025, showcasing strong financial performance despite a challenging macroeconomic environment. The company’s stock closed at $88.50, experiencing a modest 1.15% decline in aftermarket trading, suggesting investors may have had higher expectations despite the solid results.

The presentation positioned Workiva as the only platform for assured integrated reporting in a total addressable market (TAM) of $35 billion, spanning financial reporting, governance, risk and compliance (GRC), and sustainability management solutions.

Quarterly Performance Highlights

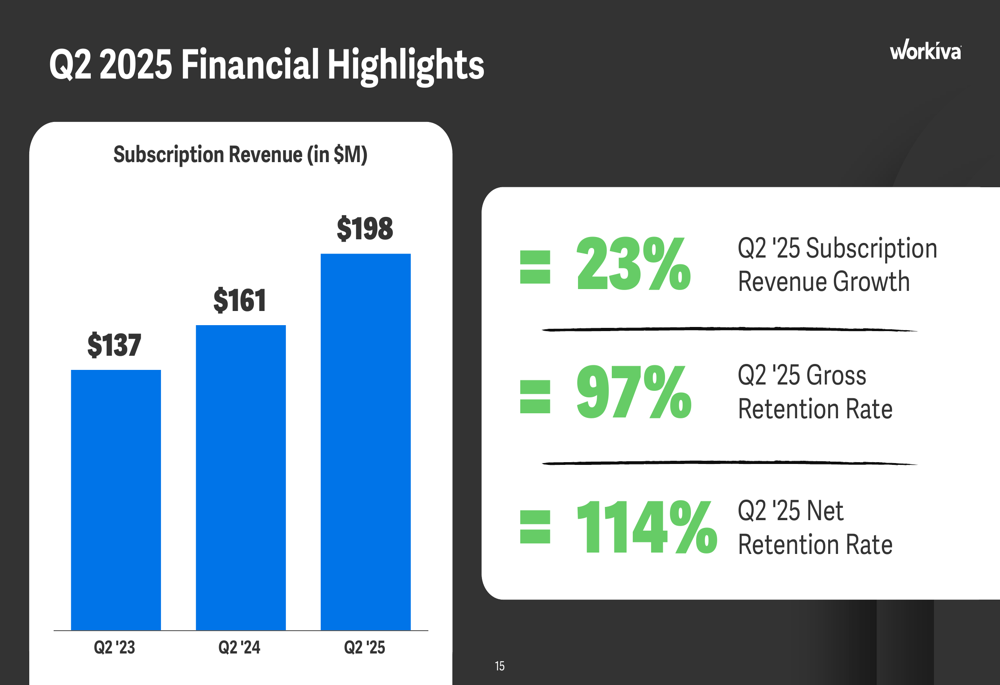

Workiva reported substantial growth in Q2 2025, with subscription revenue increasing 23% year-over-year to $198 million, up from $161 million in Q2 2024 and $137 million in Q2 2023.

As shown in the following chart of quarterly subscription revenue growth:

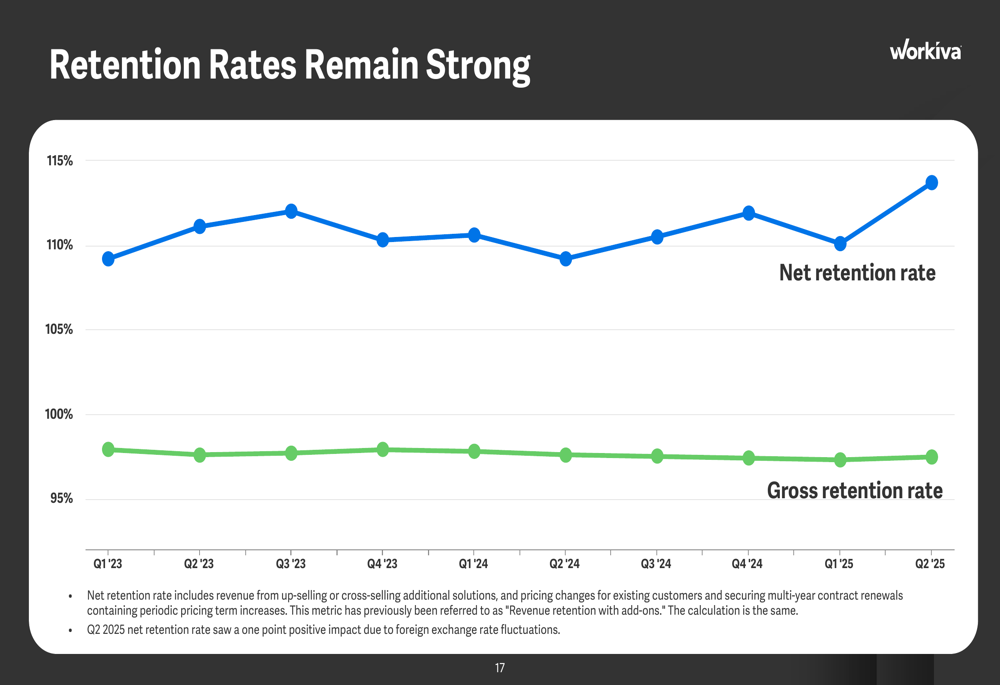

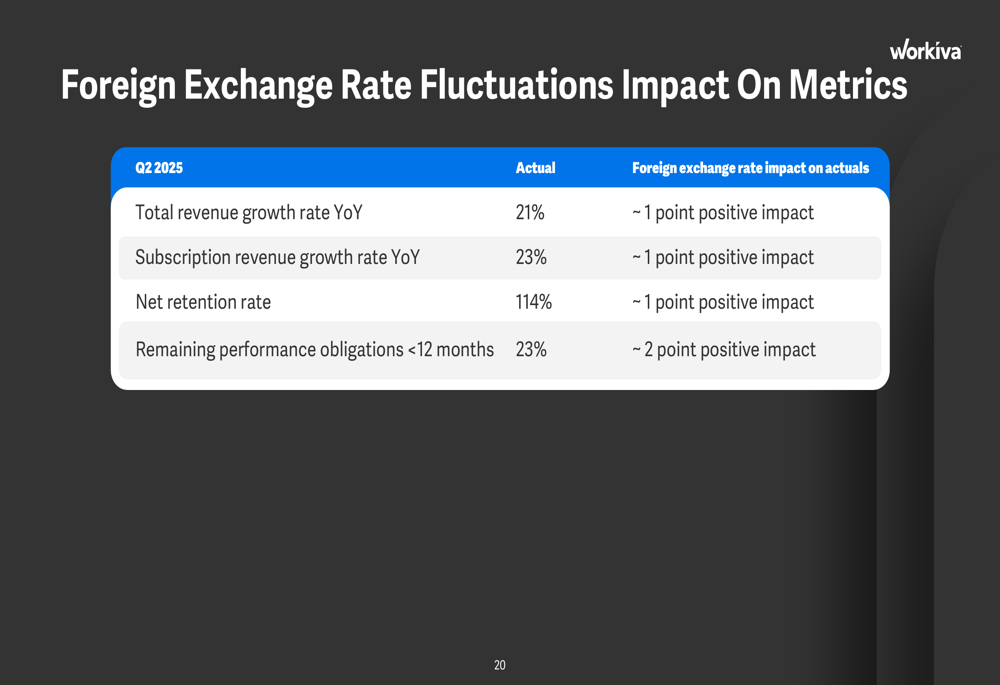

The company maintained impressive customer retention metrics with a 97% gross retention rate and 114% net retention rate, indicating strong customer satisfaction and expansion within existing accounts.

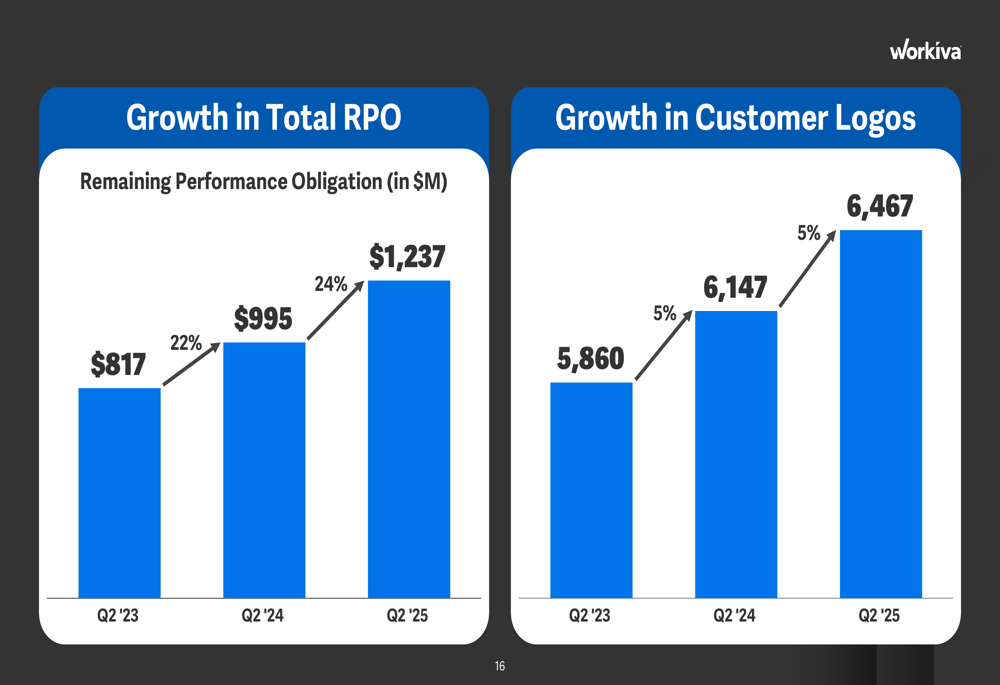

Total remaining performance obligations (RPO) reached $1.237 billion in Q2 2025, representing 23% year-over-year growth from $995 million in Q2 2024.

The following chart illustrates this growth alongside the expansion of Workiva’s customer base:

Strategic Initiatives

Workiva’s platform strategy continues to gain traction, with 71% of subscription revenue now coming from multi-solution customers, up from 67% in Q2 2024 and 62% in Q2 2023.

This trend is clearly demonstrated in the following chart:

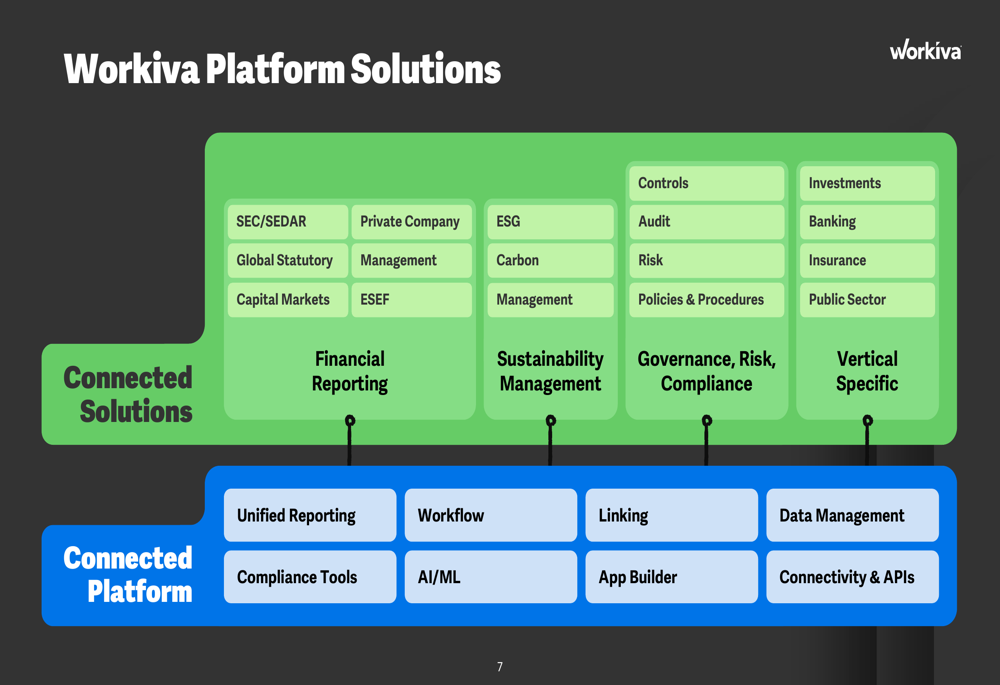

The company’s platform approach addresses the growing complexity in reporting requirements through an integrated solution set spanning financial reporting, sustainability management, and governance, risk and compliance.

Workiva’s comprehensive platform capabilities are illustrated in this overview:

The Q2 earnings call revealed that while the financial services vertical showed exceptional growth, the sustainability segment experienced some slowdown. CEO Julie Iskow addressed this during the call, noting, "Sustainability is only 20% of our TAM and it’s less than 15% of our revenue," suggesting the company’s diversified approach provides resilience against fluctuations in any single segment.

Detailed Financial Analysis

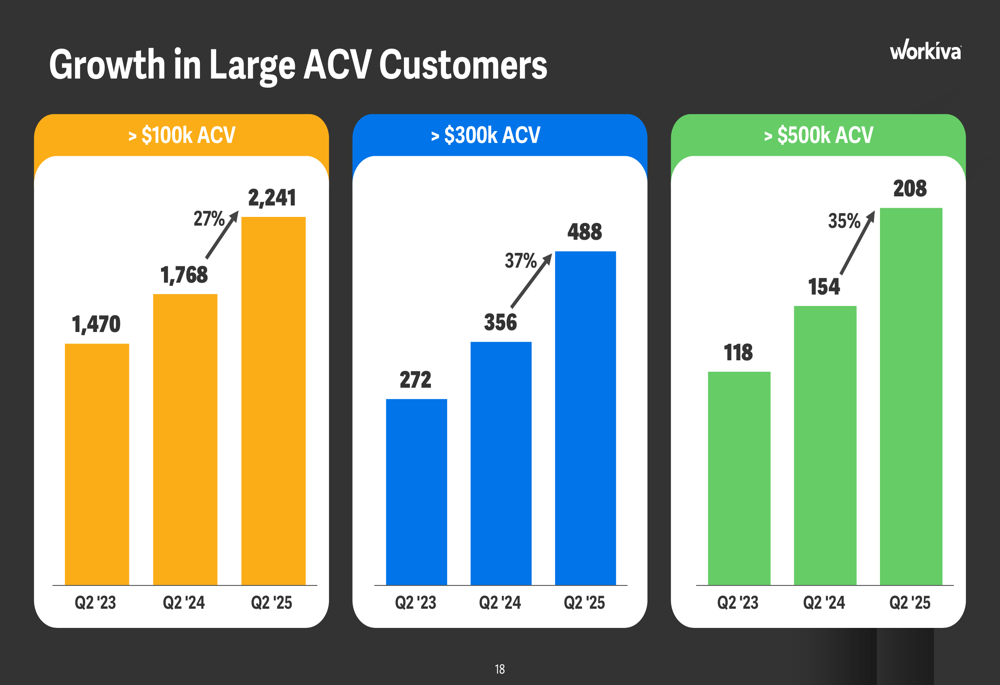

Workiva continues to expand its presence among higher-value customers. The number of customers with annual contract value (ACV) exceeding $100,000 grew to 2,241 in Q2 2025, up from 1,768 in Q2 2024 and 1,470 in Q2 2023. Similar growth was seen in the $300,000+ and $500,000+ ACV segments.

The following chart details this upmarket movement:

The company highlighted several significant deals in Q2 2025, including a seven-figure expansion with a US-based Fortune 500 bank that purchased Bank Regulatory Reporting, Sustainability Reporting, and Workiva Carbon solutions. Another notable win was a mid-six-figure deal with a South American utility company that purchased five solutions across Workiva’s platform.

Forward-Looking Statements

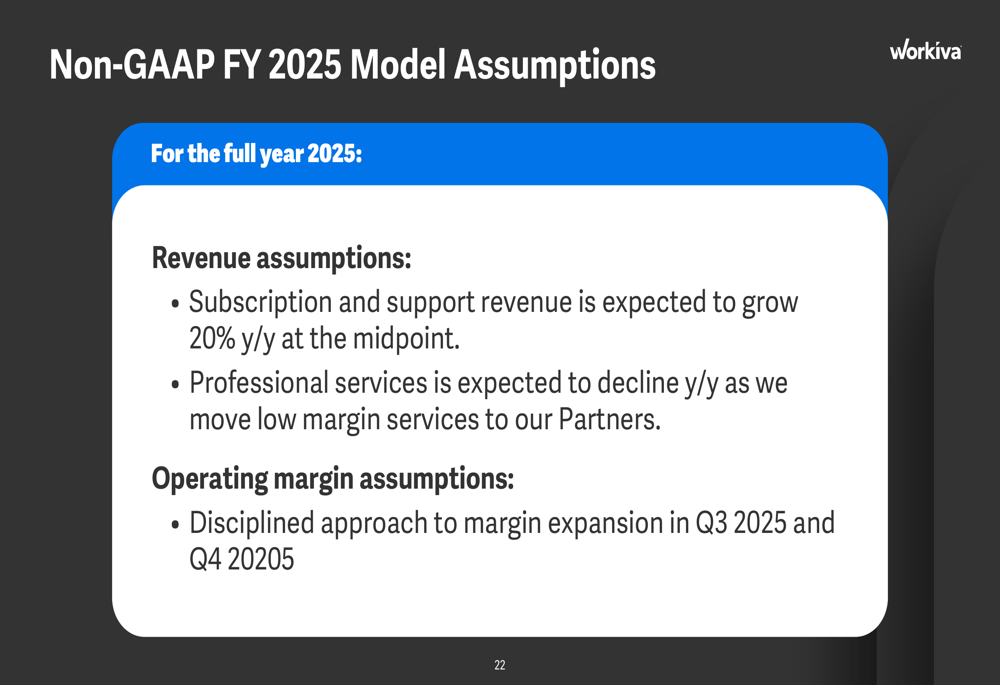

For Q3 2025, Workiva expects total revenue between $218 million and $220 million, representing 17.4% to 18.5% year-over-year growth. The company projects a non-GAAP operating margin of 7.0% to 8.0%.

For the full fiscal year 2025, Workiva forecasts:

- Total revenue of $870 million to $873 million (17.8% to 18.2% year-over-year growth)

- Non-GAAP operating margin of 7.0% to 7.5%

- Non-GAAP EPS of $1.31 to $1.38

The complete guidance summary is presented below:

Looking further ahead, Workiva outlined its medium and long-term operating model, showing a path to significant margin expansion. The company aims to increase its non-GAAP operating margin from 2% in 2023 to approximately 16% by 2027 and 24% by 2030, primarily through gross margin improvement and operational efficiencies.

This progression is detailed in the following chart:

Competitive Industry Position

Workiva positions itself as a leader in a $35 billion total addressable market, with Financial Reporting representing 50% of the opportunity, while GRC and Sustainability Management each account for 20%, and Industry Vertical solutions make up the remaining 10%.

The company’s market opportunity spans multiple regions, with the Americas representing $16.4 billion, Europe $10.9 billion, and APAC $7.7 billion of the total TAM.

During the earnings call, executives emphasized their focus on expanding customer relationships and optimizing sales and marketing investments. The company is transitioning to a hunter-farmer sales model, which could present execution challenges but aims to improve efficiency in the long run.

Conclusion

Workiva’s Q2 2025 presentation demonstrates continued strong performance with 23% subscription revenue growth and increasing customer adoption of its multi-solution platform. While the stock experienced a slight decline following the results, the company’s consistent execution and clear path to improved profitability suggest a solid foundation for future growth.

The company faces some headwinds from macroeconomic uncertainties and a moderate slowdown in the sustainability segment, but its diversified approach and strong retention metrics indicate resilience. As Workiva progresses toward its long-term margin targets, investors will be watching closely for continued execution on both growth and profitability initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.