Proactive Investors -

- FTSE 100 well above session low of 7,453.69

- US stocks seen touch higher as earnings flow

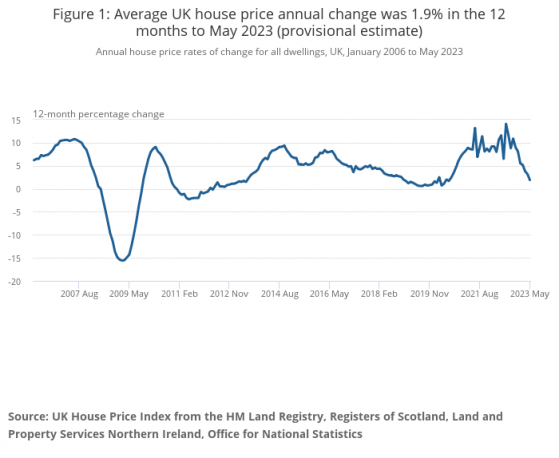

- UK CPI eased to 7.9% in June, lowest level since March 2022

US housing starts miss

US housing starts fell by 8.0% to 1,434,000 in June, below the consensus forecast for 1,480,000, with net revisions at -64,000. Meanwhile, building permits dropped 3.7% to 1,440,000, also below the consensus forecast of 1,490,000.

Kieran Clancy, senior US economist at Pantheon Macroeconomics commented: "The drop in June starts reverses only part of the 16% surge in May; the upward trend remains intact. Month-to-month noise aside, a divergence is emerging between rising single-family starts, tracking the ongoing rebound in new home sales, and falling multi-family starts, following the downshift in rent inflation. We expect both trends to continue over the next few months, but the net result will still be an increase in total residential construction spending, because single-family units account for a much larger share of total activity."

He added: "The drop in headline June starts is due to a 7% fall in single-family starts and a 9.9% plunge in the multi-family component. Both overshot the level implied by permits in May, so a correction was always likely. That said, single-family starts reversed only part of the May surge, and permits rose 2.2% in June, leaving them 23% above their recent low in December 2022. The rebound in single-family starts is being driven by a lack of existing home supply, which is boosting new homes sales even as aggregate mortgage demand continues to bounce around the cycle low.

"The drop in June multi-family starts, by contrast, reverses all the May jump, and the 12.8% decline in multi-family permits point to further declines in starts in July and August. Soaring growth in rents led to a boom in multi-family construction in 2021/early 2022, but growth in rents on new leases has since rolled over, and is driving multi-family starts back towards their pre-Covid level."

Energy switching jumps

June marked a jump in the number of households switching energy suppliers as market competition heated up thanks to falling prices, according to a report by Energy UK.

Some 170,636 customers switched to a new supplier last month, up 77% on a year earlier when firms were reluctant to offer competitive deals due to higher wholesale energy costs.

57% of the switches were between larger suppliers, including British Gas, Bulb, EDF (EPA:EDF), E.ON, Octopus, OVO and Scottish Power, according to industry body Energy UK.

Smaller and mid-sized suppliers made leeway though, gaining 4,747 new customers over the month, equating to around 3.3% of switches.

“It is worth noting that this data is from the last month before the price cap fell below the Energy Price Guarantee,” Energy UK said in its report.

A look at today’s fallers and risers

Fallers

Watkin Jones - down 39% to 46.9p: Shares plummeted on Wednesday as the UK residential rental property firm issued a profit warning and said its chief executive Richard Simpson has stepped down with immediate effect. Multiple previously announced property deals are now in question as a result of higher interest rates and prevailing economic uncertainty, with the company warning of “a greater degree of risk” to transactions completed by the year’s end.

Risers

Ariana Resources - up 15% to 2.48p: Shares jumped as it confirmed construction work had resumed at the Tavsan mine in Turkey after a court ruling in favour of partner and operator Zenit. Work at the project had been halted while the Administrative court in Kütahya considered environmental concerns raised in the local community.

Cohort - up 9.8% to 489p: Shares in the management consulting company jumped after preliminary results showed an increase in profits and revenues. Sales in the year to 30 April 2023 grew by 33% to £182.7mln, while the firm posted a record adjusted operating profit of £19.1mln.

US preview

US blue chips are expected to start a touch higher on Wednesday, consolidating after the Dow Jones Industrial Average (DJIA) posted its longest winning streak since March 2021 in the previous session, with another flood of corporate earnings to dominate attention.

In pre-market trading, futures for the DJIA were 0.1% firmer, while those for the Nasdaq 100 also added 0.1%, but contracts for the S&P 500 edged 0.02% lower.

On Tuesday, the DJIA notched up a seventh straight positive session, rising 366.58 points, or 1.1% to close at 34,951, while the S&P 500 gained 0.7%, and the Nasdaq Composite added 0.8%. All three major averages recorded their highest closes since April 2022.

The US second-quarter earnings season has got off to a good start - of the 38 companies in the S&P 500 that have reported results so far, 82% have exceeded expectations, according to FactSet data.

On the earnings slate for Wednesday, Goldman Sachs (NYSE:GS) is set to report before the opening bell, while Netflix (NASDAQ:NFLX), Tesla, IBM (NYSE:IBM) and United Airlines will post earnings after the close.

On the data front, June housing starts, which will be released at 8.30am ET, are expected to have dropped by 9.3%, according to economists, down from the big 21.7% jump posted in May.

Meanwhile, June building permits are anticipated to have declined 0.7%, according to Dow Jones consensus estimates. That would be down from a 5.2% gain the previous month.

TickMill Group’s market analyst Patrick Munnelly commented: "Stateside, the housing sector has been impacted by higher interest rates, and today's housing starts and building permits data will provide insights into the sector's recent performance.

"Yesterday's retail sales report showed resilient consumer demand, and market participants will be interested to see if the housing data support that trend."