Archer-Daniels-Midland (NYSE:ADM) is a major agricultural commodities firm. Through processing, storage, transportation, marketing, and trading, the company is active at many points in the production and delivery of plant-based nutrition for humans and animals, along with biofuels and industrial products.

Source: ADM

ADM reported strong earnings for Q1 and Q2 of 2021, and will be reporting for Q3 on Oct. 26. For Q1 and Q2, EPS beat forecasts by 33% and 29.4%, respectively. The expected EPS for Q3 is equal to the reported earnings for Q3 of last year. ADM has beaten expectations for the past 8 quarters. Given the inflationary environment for food, a beat for Q3 seems quite probable.

Source: ETrade. Green (red) numbers are amount by which EPS exceeded (missed) consensus expected EPS.

The YTD and 12-month total returns for ADM are 27.8% and 32.6%, respectively. The current share is 6.4% below the 12-month high close of $68.77 on June 4, 2021.

Source: Investing.com

Rising inflation and interest rates favor ADM and part of the gains in the stock reflect investors building positions in companies expected to provide a decent hedge against inflation. ADM also has a constituency of income-oriented investors who place a premium on the company’s long-term commitment to the dividend. The company is a Dividend Aristocrat, with 27 years of consistently increasing its dividend.

With a yield of 2.34% and 3- and 5-year dividend growth rates of 3.5% and 4.5%, respectively, the Gordon Growth Model yields expected annual returns in the range of 5.8% to 6.8%. The falling dividend growth rate in recent years suggests caution in extrapolating past dividend growth rates into the future, however.

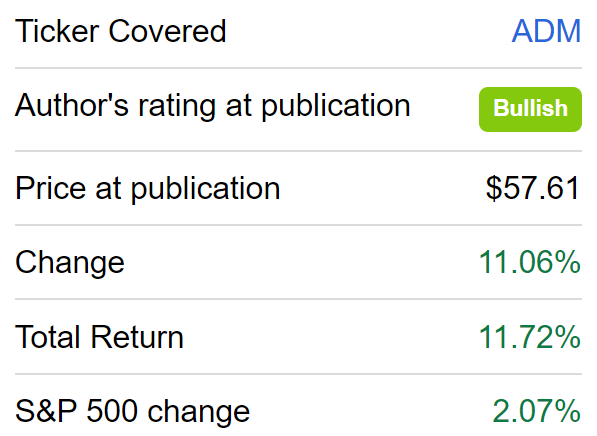

Since I last wrote about ADM on July 17, at that time, ADM had fallen 15% from its YTD high as concerns about inflation eased. The Wall Street consensus for ADM was bullish, with a 12-month price target that was 20% above the share price at that time. The implied outlook from options prices (aka the market-implied outlook) was modestly bullish and the implied volatility was 24%. The overall picture for ADM looked favorable and I assigned a bullish rating.

Source: Seeking Alpha

In the (almost) 3-month period since I wrote that post, ADM shares have risen by 11.1% vs. 2.1% for the S&P 500. The concern, looking forward, is whether too much of the expected earnings growth is now reflected in the share price. In addition, over this period, the Wall Street consensus price target for ADM has fallen somewhat. ETrade’s calculation of the Wall Street consensus 12-month price target is down by about 8% since mid-July, for example.

Most readers will be familiar with the Wall Street analyst consensus, but many will not have encountered the market-implied outlook derived from options prices. The price of an option on a stock reflects the options market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the strike price) between now and when the option expires.

By analyzing the prices of options at a range of strikes and the same expiration date, it is possible to calculate the probabilities of all possible future returns that will reconcile the options prices. The results are a probabilistic outlook for the stock price that reflects the consensus views of buyers and sellers of options. This is the market-implied outlook. For more background and links to the relevant financial literature, see this post.

With the rapid gains in ADM and the reduced consensus price target, I have calculated the market-implied outlook for ADM using current options prices to determine whether ADM has sufficient potential upside to merit a buy rating.

Wall Street Analyst Outlook

ETrade calculates its version of the Wall Street consensus using ratings and price targets from ranked analysts (rankings determined by TipRanks) who have published their views within the past 90 days. The current consensus is based on the views of only 3 analysts, as compared to 8 when I analyzed ADM in July. The consensus rating is bullish and the consensus 12-month price target is $65, as compared to $70.8 in mid-July. The expected 12-month price appreciation with this target is 1%.

Source: ETrade

Investing.com calculates the Wall Street consensus outlook for ADM from a group of 15 analysts. With this larger sample, the consensus rating is also bullish and the consensus 12-month price target is $67.54. With the dividend yield of 2.34%, the expected total return is 7.3%, very close to the estimated total return using the Gordon Growth Model and the 5-year dividend growth rate.

Source: Investing.com

While the small sample of analysts in the ETrade consensus is a red flag, the overall outlook is generally consistent with the Investing.com results. Both are bullish, with low expected price appreciation for the next 12 months.

Market-Implied Outlook For ADM

I have analyzed put options and call options at a range of strike prices, all expiring on Jan. 21, 2022, to generate the market-implied outlook for the next 3.3 months (from now until the expiration date). I have also analyzed options expiring on Mar. 18, 2022 to calculate the market-implied outlook for the next 5.2 months.

I would have preferred to look closer to mid-2022 for the longer-dated outlook but there are currently no options expiring in 2022 other than those in January and March. The options expiring in January are considerably more liquid than those expiring in March, so the 3.3-month outlook is considered more robust as a consensus view.

The standard presentation of the market-implied outlook is in terms of probability distribution of price return, with probability on the vertical axis and return on the horizontal.

Source: Author’s calculations using options quotes from ETrade

The market-implied outlook for the next 3.3 months is fairly symmetric, but the peak probabilities are tilted towards positive returns. The maximum probability corresponds to a price return of +3%. The annualized volatility derived from this distribution is 25%, which is quite low for an individual stock.

To make it easier to directly compare the probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Source: Author’s calculations using options quotes from ETrade. The negative return side of the distribution has been rotated about the vertical axis.

Viewed in this way, the probabilities of positive returns are consistently higher than for negative returns of the same magnitude across a range of the highest-probability outcomes (the blue curve is consistently above the red dashed line). This is a bullish outlook. There are slightly elevated probabilities of negative returns for large-magnitude outcomes, but these occur at a low probability overall.

The market-implied outlook to March of 2022, calculated using options that expire on Mar. 18, 2022, exhibits probabilities of positive and negative returns that are much closer to one another (less bullish, more neutral). The maximum probability corresponds to a price return of -5.5%, which is bearish. The annualized volatility derived from this distribution is 26%.

Theory suggests that the market-implied outlook will tend to have a negative bias because investors, in aggregate, are risk averse and will tend to pay more than fair value for put options. As such, a market-implied outlook with matching probabilities of positive and negative returns (the solid blue line and the red dashed line are very close to one another) is interpreted as mildly bullish but the negative peak probability is somewhat bearish. Given the liquidity of the March options is thin, the only takeaway from this outlook is that it is generally neutral.

Source: Author’s calculations using options quotes from ETrade. The negative return side of the distribution has been rotated about the vertical axis.

The market-implied outlook to Jan. 21, 2022 is modestly bullish, shifting to be more neutral by mid-March. The market-implied outlook for Jan. 21, 2022 is slightly more bullish than it was in July and the volatility is about the same.

Summary

Investors, in aggregate, have driven up ADM’s share price in response to higher realized and expected inflation, especially in agricultural commodities. The question is whether the share price has reached the point that there is little upside remaining.

The Wall Street consensus is that the next 12 months of potential gains are largely priced in and that expected total return for ADM is in the range of 5%-6%. The Wall Street consensus rating continues to be bullish, even though the price target implies that 12-month appreciation potential is low.

The current yield and dividend growth rate, if we are willing to extrapolate from recent years for the growth rate, can reasonably support expected return of 5.8%-6.8%. The market-implied outlook to mid-January is slightly more bullish than it was a couple of months ago and the expected volatility from that outlook is 26%. Expected returns in the range of 5%-7%, encompassing the Wall Street consensus and Gordon Growth Model estimates, are not attractive at this risk level.

For a buy, I generally look for expected return of at least half the volatility and ADM does not come close to this threshold. With its beta of 0.86, ADM will tend to have some portfolio benefits so the stock does not need to look terribly attractive on a standalone basis.

Even though the expected upside for ADM is very limited, the bullish Wall Street consensus, the bullish market-implied outlook to early next year (albeit looking more neutral later), and the potential for continued high food inflation, convince me to stick with my bullish rating for ADM.